Perfect Streams Forever

Insights into the unmet needs of music streaming subscribers

When consumers are having to make tough choices, how can music streaming brands deliver more value to keep and attract new paying subscribers?

In early 2023 we conducted an in-depth survey plus video interviews with music app users to discover what they value most. This online report presents a summary of the opportunities we identified for streaming services and music brands.

Read on to find out what we discovered…

Introduction

As the cost of living rises and budgets become stretched, the growth trajectory of the paid music streaming market will not be spared disruption from consumer cutbacks.

But with opportunities to deliver greater value being plentiful, could the risk of being dropped be averted, at least partially, by a renewed focus on subscriber needs?

In late 2022, with inflation soaring and consumer confidence in free-fall, many people are looking to cut-back on spending and will have to make hard choices about the services they continue to pay for. Entertainment streaming subscriptions, including music, are no longer immune to this, especially as those who choose not to pay can downgrade to free ad-supported services.

Our research shows the impact of this tightening of belts, with one in five paid music streaming subscribers saying they are considering cancelling in the year ahead. On the current path, we can expect a downturn in the growth of paid music subscribers - with both retention and acquisition impacted by a more prudent and thrifty audience.

“Reduce the price. With everything going up I would rather not pay and listen to ads if the price keeps going up”

“Provide more value for people and show what you’re doing to combat the cost of living crisis. These apps aren’t a necessity...”

“Keep costs as low as possible to help with rising inflation costs!”

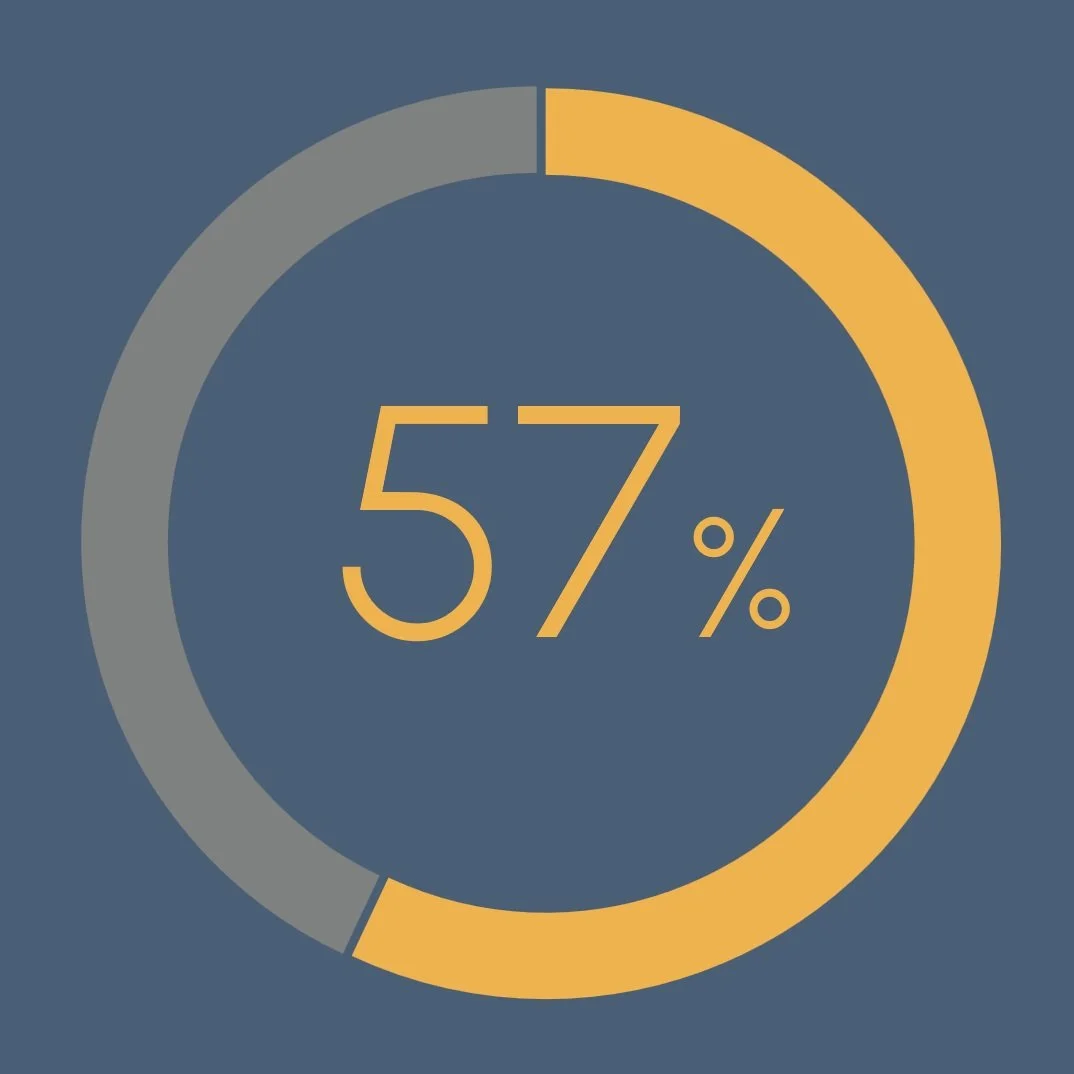

Cancellation consideration

% subscribers either ‘very likely’ or ‘quite likely’ to cancel in the coming 12 months.

What can streaming music brands do to fight back?

In the months ahead, users will be taking a closer look at what streaming services offer and how well they reflect the outcomes they as music consumers are seeking.

Delivering more value, in alignment with digital music listeners’ needs, should remain central to any strategies that seek to build a loyal and paying customer base. Our research surfaced seven underserved needs that could each act as potential springboards for product strategy.

Read on to discover what we’ve learned…

Provide more choices than

full premium or free

01

Times are tough, cancellations are coming.

Many music fans who are looking to save money would favour a mid-priced, full-featured, ad-supported tier over cancelling. They don’t have that choice yet.

Limited subscription choices do not meet all listener needs and miss out on potential revenues

During turbulent times, when consumers are having to justify how and where they spend their money, the current take-it-or-leave-it approach to music subscriptions may not serve users’ or brands’ needs fully. Taking the market leader Spotify as an example, today in Autumn 2022, the options are either a fully-featured premium subscription (without ads, starting at £9.99 for most) or a free ad-supported model with a limited feature set (no offline listening, limited song-skips and shuffle-based listening). With some users struggling to pay for a subscription their only real choice is downgrading to the free ad-supported tier and the disappointment of losing all the premium features they’ve come to value.

And the brands that do have lower priced tiers today come with some big limitations, making them only suitable for casual listeners: Amazon has a shuffle-only offer that is ‘free’ for Prime subscribers and single Echo device plans for £3.99pm, Apple has Music Voice for £4.99 which only works via Siri voice control.

Given a choice many would go mid-tier

There appears to be a missed opportunity for a mid-tier offering at a lower price; ad-supported but with a more fully-featured user experience. Asked to make a hypothetical choice between the current market offer and a new tier that combines ads and being fully featured, this potential third tier has the most appeal to consumers (chosen by 44%). However, a clear generational difference exists, with younger listeners as likely to choose premium (40% of those aged 18-34s) as a mid-tier subscription (39%) - though most still choose ad-supported tiers to cut costs.

“Price is driving every decision I make. If the cost was a little lower, or if there was a ‘mid-range’ subscription, I’d consider resubscribing.”

“Have a slider choice. More ads reduce monthy cost, less increase monthy cost up to zero ads. Allow users to select and flex this as required”

How users would feel if they lost their subscriptions:

Free

With adverts Limited features

Agree:

They would be disappointed to lose access to their Spotify Premium subscription (Spotify subscribers)

What consumers would choose if a mid-tier subscription with adverts was available:

Mid-priced

With adverts

Fully-featured

Premium-priced

No adverts

Fully-featured

Spotify and others have piloted blended paid & ad-supported packages like this but none have yet to make it to market. It could be that the risk of cannibalisation of premium tier subscribers and revenues was too high. However, with increased pressures on peoples’ entertainment budgets and Netflix recently setting a precedent for such a package, in the video space, that calculation will likely be revisited. If it doesn’t come from Spotify, this gap in the market could prove an opportunity for plucky competitors looking to attract listeners who are feeling the squeeze on budgets.

Keep the tunes &

the artists fresh

02

Familiarity fatigue is setting in.

A large number of users feel they hear the same artists and tracks too often in playlists and recommendations. The lack of fresh music weakens subscription value.

Providing variety and bringing new artists and songs to the attention of listeners is crucial to maintaining interest and delivering value.

Playlists can feel stale & over familiar

Many users of streaming music apps become frustrated with hearing the same artists and songs too often in playlists. Whilst music streaming apps are mostly rated positively on delivering variety, few can be considered great. Less than one in three users rate them as ‘very good’ or better on variety and two in five feel they hear the same songs too often in playlists.

For some, the repetition of a narrow set of genres, artists and tracks they experience from streaming services feels too close to the playlists of commercial radio. It does not reflect the full diversity of genres and mix of new and older tracks that they would expect from streaming services. This limits the value they receive from what should feel like an endless library of potential new artists and songs.

“Keep recommending new music to customers. It sometimes seems like a lot of effort to find new music”

“Provide more variety, more diversity - throw in occasional different songs to choose from”

“Balance music between vintage, popular and modern and genres - folk, country, rock, metal, punk, etc”

Key attitudes and ratings on music app variety:

Agree

I hear the same songs too often in playlists

Agree

There is a lack of variety in the recommendations on music apps

% Rate apps Excellent / Very good on:

Playlists are always varied and interesting (app average)

New music is not given enough prominence for some

For many music fans the pleasure they get from music comes from the thrill of hearing new and emerging artists. But whilst streaming services have a good track record for introducing listeners to new releases, some still feel that established bands and artists are being given too much screen or ‘air-time’ on the apps they use. This weakness was raised amongst users of all music apps but appears notably more top of mind for Apple and Amazon Music users.

“Take me away from my usual playlists. I want new stuff that challenges me a bit”

“Offer more choice from lesser-known bands and artists”

“I would like to see more obscure songs that I like featured on the app”

Reflect users’ tastes,

in all their diversity

03

Recommendations are hit-and-miss.

The full breadth of music styles listeners like is not always reflected in the app experience. Promoted content is too often irrelevant and disrupting.

With most streaming music users not feeling that recommendations match their tastes, there is more that can be done to personalise and align content suggestions

Recommendation experience underperforming

Whilst above average in terms of importance to music app users, the suitability of recommendations performs below par when we asked users to rate quality. There are many examples of good recommendations, and most users are positive (74%), but there are also many recommendation misfires where the algorithms get it wrong. As a result, just one-third say the music app they use is either ‘Excellent’ or ‘Very good’ at providing recommendations that closely reflect their tastes.

“I find the suggestions are about 50/50 of what I actually listen to vs. current music that I’m not interested in.”

“They need to target the genres of music to the subscriber. Listen to what the subscriber likes”

How app users rate recommendation fit

Rate ‘Excellent’ or ‘Very good’ for:

Recommendations closely reflect my tastes

Promoted content causes friction if not personalised

Whether it’s major artist releases or the latest high profile celebrity podcast, pushed content that does not align with users’ interests can detract from the personalised experience premium users expect. Overall, two in five felt that there was too much promoted content on the apps they use. Amazon and Apple Music subscribers in particular feel that their own music tastes are not as central to the content experience and recommendations as they would like. Those with less mainstream tastes were notably more likely to be annoyed by some of the pushed content they see presented.

Attitudes towards the amount of promoted content

Agree

There is too much-promoted content on music apps

“They need better algorithms for suggestions to users rather than pushing whatever you believe should sell well”

“To make the music relevant to the listeners tastes and not fill with stuff that has no relevance or place”

Involve & engage users

in music discovery

04

Users seek more active personalisation.

Listeners don’t want to be beholden to algorithms alone. They want enhanced discovery features, more content control and insights into their own listening

Some listeners would like a more active and engaging music discovery journey that blends personalisation, content insights, expert curation and algorithms

Better music discovery features are wanted by most

Improved features and user experience for discovering new music was one of the most popular development areas explored in our research - appealing to users of all music apps. Younger users, those aged under 35, in particular, called for music streaming apps to improve the features and experience in this area (80% interested).

Some users would like to collaborate with algorithms by actively picking and choosing the genres, artists and songs they like so they could get a more personalised experience: more accurate, more varied and more engaging. Others would like to learn as they discover new music: who are the original, leading and emerging artists within a genre, what are the best tracks to listen to and what is most popular.

Interested in:

Better music discovery features

“Space to tailor your favourite artists, albums and genres so you get more targeted recommendations (not solely based on what you’ve listened to) ”

“Have a dedicated music introduction area to help users find new genres, bands, learn and feel a part of music scenes...”

There is huge interest in personalised music charts

Charts, based on personalised listening habits, were the most popular feature we tested (82% interested) and indicate the potential for enhanced music choices led by insightful usage data. Spotify Wrapped, that provides listeners with a yearly summary of their listening habits, is an annual highlight for many of its users - some would like access to information like this as an always-on benefit. These charts could be used (and shared) as jumping-off points for content users know they are likely to enjoy.

A role for both algorithms and curation

And users would like a human element to their music discovery, with two in five saying they prefer playlists created by other people to those created by algorithms. When tested, interest in playlists curated by artists, DJs or celebrities appeals to half of users, rising to almost two in three (64%) amongst the under 35s.

Discovery features of interest to users:

Interested in:

My top listening charts, e.g. songs / artists / genres

Interested in:

Celebrity / artists / DJ curated playlists

Help users get lost in the music they love

05

Music is much more than audio.

Fans want to immerse themselves in the cultural eco-system of music. They want to hear, watch and read more about the genres and artists they love.

The opportunity exists to augment the listening experience with related content and features that align with music fans’ passions.

Music content of interest goes wider than songs & audio

Music fans can be an obsessive bunch, craving information and insight into the music and artists they love via a range of media formats. Whilst users want music discovery and listening to be central to their music app experience, and bloat should be avoided, there is significant interest in a range of complementary content for music fans. Official music videos, already available with Tidal and YouTube Music, topped the list of features that appealed (66% interested) and there was interest from around half respectively in streamed sessions and gigs, presented music shows and artist interviews.

% Interested in each feature

“I’d like there to be different recordings of the same song, preferably a good selection of quality live recordings”

“Have involvement, articles and videos from artists and journalists about what’s going on in the music world.”

“I would encourage them to widen to including music videos and have the ability to get songs before they are released ”

Social streams and communities appeal to younger users

Whilst social and user-generated content and features appear to be niche - not coming up spontaneously and having lower appeal vs. professionally produced content - it does hold some potential amongst younger audiences. More than half of those aged under 35 respectively find either user-generated content (e.g. cover versions, reviews or reaction videos) or communities and chat about artists appealing.

% Interested in each feature

Present music at its very best

06

High quality audio is expected by paying users.

The ability to listen to pristine audio, as the artist intended, is an experience many crave. But they won’t always pay extra for it – HiRes premiums may backfire.

Whilst largely dependable, not all online music services are presenting recordings at the quality level users want

Better quality audio appeals though most wouldn’t pay

Many users want to experience music in the best quality they can – getting as close as possible to the audio that artists intended and making the most of the speakers and headphones they’ve invested in. However, the experience across the market is mixed; HiRes audio is available with some providers (Apple, Amazon, Tidal, Qobuz) but despite promises, has yet to roll-out on Spotify though there has been some recent noise on that front.

Overall, most users of music streaming services (65%) are interested in improved audio quality. However, for most it is not something they would pay extra for, with just over one-third (37%) agreeing they would be willing to do so.

Younger audiences place more value in getting better audio quality, with demand for Hi-Res quality (75% interested) and the willingness to pay for it (47%) notably higher.

“Make high quality audio a standard feature”

“They should all offer the best audio quality available.”

Demand for better quality audio:

INTERESTED IN:

Improved sound quality, e.g. HiRes, Spatial audio

AGREE:

I would pay more for higher audio quality

Aged 18-34 = 47%

Potential for streaming services in the hardware space

The desire for better quality audio also extends to streaming brands offering hardware that delivers the best listening experiences. Three in five say they would be interested in speakers or headphones from streaming services that improve the listening experience.

Apple and Amazon are of course already active in this space but this research suggests that there could also be potential for the pure streaming brands, like Spotify, to invest more in hardware.

INTERESTED IN

Hardware to improve listening experience, e.g. headphones, speakers

Men = 66%

Enable artists to

make a fair living

07

No streaming without rewarded musicians.

Paying artists ’fairly’ is an undying call made spontaneously by many music fans. Features that empower artists to sell merch, tickets and exclusives add value for all.

Fairer reward for artists is called for spontaneously by many, with some worrying their favourite artists could leave the platform in favour of others with better royalties

Many feel the current model is unfair to artists

Artists’ views on the royalties they receive from streaming, particularly Spotify, are well-known and are cemented in the minds of many users. As a result, many agreed that music apps don’t share profits fairly with the artists themselves (44%). As well as a general appreciation that the artists they listen to need to be able to make a living from music, some also worry about some of their favourite music being removed. As music fans they will ultimately follow the content they love.

Attitudes towards artist rewards from streaming:

Agree

Music apps don't always share profits fairly with artists

“Pay the artists a fairer percentage - the music industry is suffering badly right now”

“Pay artists fairly...the artist could pull their songs from the app and then result in me changing provider to listen to the songs I want.”

Enabling fans to support directly appeals

Beyond a hope for increase royalty payments, subscribers are also interested in features that empower artists to raise money directly from the fans. This could take the form of gig tickets (53% are interested), sales of merchandise and digital downloads (57% interested) or direct donations.

This interest is clearly reaching the bigger streaming brands already, with merch rolling out on Spotify (via Shopify) and Amazon (Artist Merch Shop), gig tickets being trialled on Spotify this Summer in the US (Live Events Feed) and Spotify’s Artist Fundraising remaining in place long after Covid.

Interested in:

Gig recommendations and tickets

Interested in:

Features to help rewarding artists & creators, e.g. merchandise, direct funding, downloads

How we conducted this research

10 Video based interviews with music subscription subscribers

Online survey with 1,000 participants who are representative of the UK online population. Conducted via the Research Bods online panel

The feedback spanned representative users of Spotify, Amazon Music, Apple Music, Tidal, YouTube Music. Results presented are based on an average across music apps and audiences

All research fieldwork and analysis was conducted in early 2023

Waveform Insight Ltd, 2023, all rights reserved. All data, unless specified, is proprietary and not for redistribution or reference without prior permission and attribution. No warranties, guarantees or liabilities apply to the contents and usage of this content.'